Figure it Out

What the largest non-bank HELOC lender teaches us about where financial infrastructure is going

When I’m talking to smart skeptics, people who aren’t crypto believers and don’t particularly want to be, I bring up Figure Technologies. It’s usually the moment something clicks.

Not because it’s a crypto company. Because it’s just a better business.

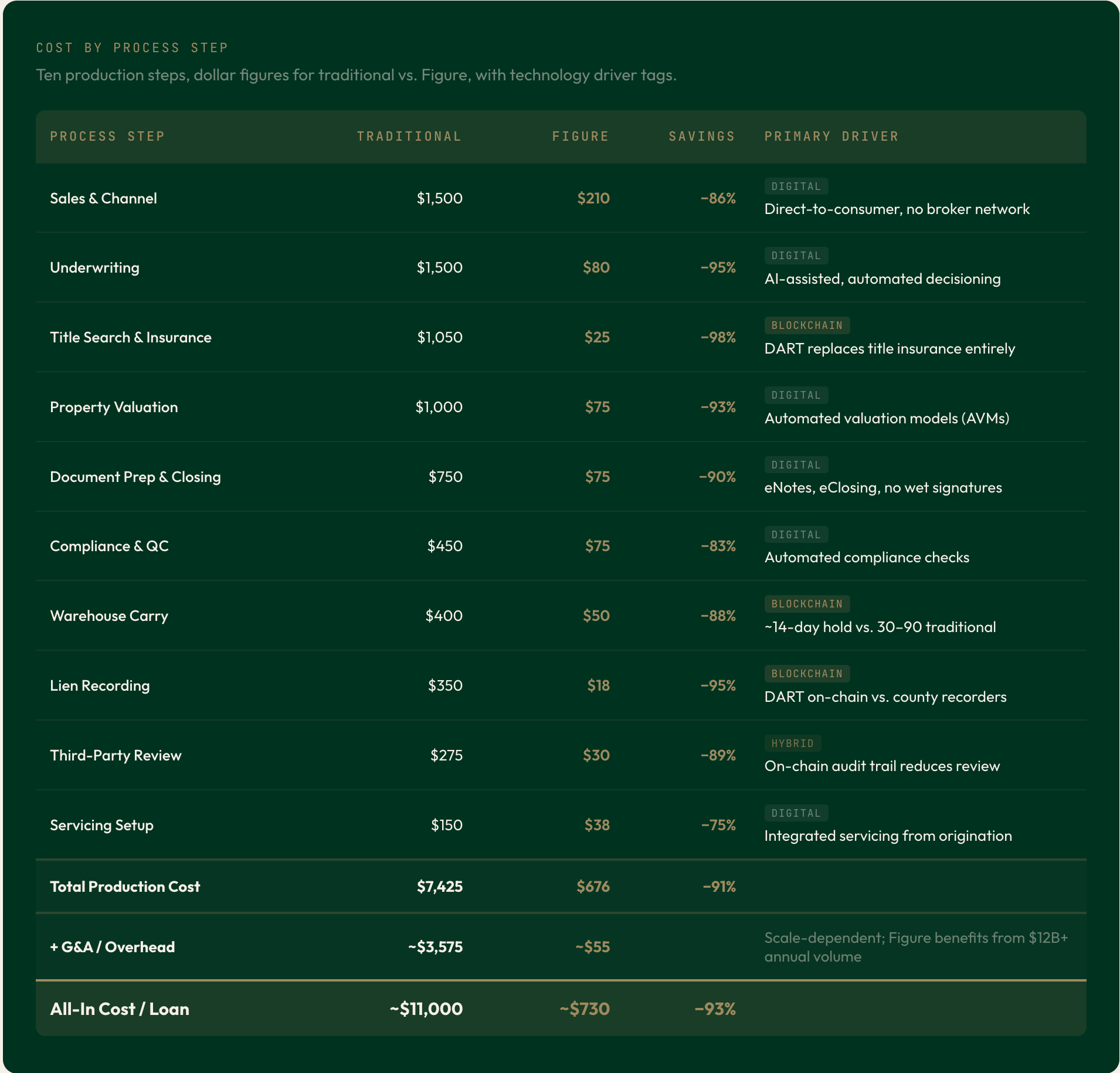

Mike Cagney knows fintech. He built SoFi before Figure. The question he asked was simple: why does it cost $11,000 to originate a home equity line of credit? Most people assume it's a regulatory or capital problem. It's not. It's technology and process. So he built the fix. Today Figure closes a HELOC in 5 days at roughly $730 per loan. The industry average is 45 days and $11,000.

He's built an $8B company out of it.

$20B+ HELOCs originated. 55% EBITDA margins. 754 average FICO. They haven’t cut corners on credit quality to drive demand. They cut costs at the technology layer.

The number that sticks with me is the break-even gap. A traditional lender needs a $367K loan just to break even on origination fees. Figure breaks even at $25K. That $342K gap isn’t a competitive advantage. It’s an entirely new market. Loans that were economically impossible to make are now profitable. That’s what happens when you structurally change the cost of production.

And it’s not just the origination side. Investors buying these loans get a better product too. On-chain settlement, no trustee, no custodian, real-time visibility into the collateral. That’s 120 to 200 basis points of net yield advantage on equivalent credit. Supply improves, demand improves. Both sides of the marketplace benefit. That’s the flywheel.

Zooming out. Tokenization, which people call Real World Assets (RWA), has been all the rage. But it has a structural problem. Most of what has been tokenized is T-bills. The demand side is real: as rates fall, the T-bill trade gets less interesting and there’s genuine appetite for uncorrelated yield on-chain. The supply side is where it gets complicated.

The classic issues are adverse selection and principal-agent. Adverse selection because the assets most likely to find their way on-chain are the ones that couldn't get funded anywhere else, not because blockchain unlocked them, but because traditional capital markets already passed. Principal-agent because when the person originating the loan doesn’t hold it, their incentive is to originate more loans, not better ones. These aren’t crypto problems. They’re finance problems. They just don’t disappear because you put the loan on a blockchain.

Figure is one of the first to bring genuinely high-quality credit on-chain at scale. 754 FICO, 50% LTV, investment-grade collateral, assets that would clear traditional credit desks. The innovation isn’t in the credit. It’s in what blockchain does to the cost and speed of producing and distributing it.

At Inversion, we ask ourselves one question constantly: why does it cost X to do Y in this industry? The answer we get most often from industry veterans is some version of: this is how it’s always been done. Or it’s regulatory. Or it’s compliance. A lot of what’s been accepted as fixed costs of doing business are now variable or optional with crypto. Figure proves that. We see an immense opportunity to take this beyond HELOCs.

We put together a full breakdown of the model, the economics, and where we think this goes. Worth a read.

Full piece: https://www.inversioncap.com/insights/figure-case

We’ll be publishing more research on the Inversion site. If that’s interesting to you: https://www.inversioncap.com/insights

1m customers data exposed. Great company.

I'm really glad you wrote this.

I first noticed Figure just looking at the top crypto assets. Usually if something pops into the top 25 I don't know it's something kind of silly that I can make jokes about. But I saw Figure and I looked it up and thought: "This sounds... reasonable?"

But why the heck wasn't it buzzier?

So then I looked into it again when I decided to buckle down and get caught up on real world assets. That led to this episode of my podcast:

https://www.frontstageexit.com/p/crypto-will-touch-grass-in-2026-thanks

I made a bunch of clips form an interview Cagney did with Unchained a while back and I included several of them show. I kind of think that part of my episode is the centerpiece.

The reason I appreciate you writing this is that I'm glad to have some social proof from someone I have faith in. Because honestly everything Cagney said made sense it's just... well the numbers are kinda crazy.

Like a $300,000+ gap in what he can profitably close and what the banks can do? That's wild.

It almost seems too good to be true, and... you know what they say.

ON THE OTHER HAND: I have bought two homes myself. They were both very very inexpensive homes (you wouldn't believe).

But the process for these very inexpensive homes was CRAZY and I thought, "Why does it have to be this way."

Knowing what I know as a tech reporter, going through the process, both times, I went through it thinking: there's no way there aren't improvements to be made here.

So... I can believe that there are a lot of efficiencies to grab. But it makes me feel better that I'm not missing something if you've taken a close look at it. It seems like a really great business and one that I'm glad has figured out a way to get this source of credit in the hands of more normal people, like me.