Stablecoins: The B2B Opportunity

Just-in-time manufacturing transformed inventory. Stablecoins enable just-in-time money.

Every year, $300 billion is extracted from commerce through credit card interchange fees. Another $25 trillion in B2B payments crawls through correspondent banking, bleeding 3-4% to wire fees, FX spreads, and settlement delays.

Stablecoins are pitched as the solution. The pitch isn’t wrong, but it breaks down on a single problem: consumer behavior doesn’t change on command.

The opportunity is real. It’s just not where most people are looking.

Disclosure: My firm invests in businesses where this thesis applies.

The Interchange Tax

Every credit card transaction carries a 2-3% fee. The merchant pays it. The consumer never sees it.

For a retailer on 5% margins, interchange consumes 40% of operating profit. For a grocer at 2% margins, it exceeds profit entirely. This isn’t a rounding error. It’s a tax set by a duopoly and passed through the economy as higher prices.

Visa and Mastercard process roughly $15 trillion in annual volume.² At a blended 2% take, that’s $300 billion extracted from commerce each year.

Why Costco Is the Exception

Most businesses absorb interchange. Costco refused.

In the early 1990s, Costco’s CFO Richard Galanti explained why they didn’t take credit cards: “Our margins are less than 2 percent on most items after overhead. The banks charge 2 percent for each transaction, so if we took cards, we’d actually be losing money on most sales.”¹

One of the most admired retailers in America built its entire model around avoiding the payment system. Cash and checks only. That’s how corrosive the interchange tax was, and still is, to business economics.

Costco spent 30 years building the leverage to negotiate down to roughly 0.4% interchange, compared to the 1.8% everyone else pays.³ No one else has matched them. Target and Walmart have tried.

This is the problem with any stablecoin thesis that depends on changing consumer checkout behavior. Stablecoins offer 0% interchange but only where both parties want it.

Why Consumer Checkout Won’t Change

Credit cards have a structural defense: rewards. That 2% cash back? The merchant funds it through interchange. High-income households favor credit cards over debit 65% to 34%. They’re not switching to stablecoins to save the merchant money.

This creates a self-reinforcing loop: merchants pay interchange, interchange funds rewards, rewards drive preference, preference forces acceptance. Stablecoins offer an alternative consumers have no incentive to use.

Any thesis predicated on consumers abandoning rewards cards is fighting entrenched behavior and misaligned incentives. The better approach: route around it.

The Math

Even sophisticated CFOs have come to accept cross-border payment friction as a cost of doing business. Wire fees, FX spreads, correspondent banking delays. These aren’t line items anyone scrutinizes. They’re buried in COGS, treated as immovable, rarely questioned.

That’s changing.

Consider a U.S. industrial distributor with $75 million in revenue. Roughly $30 million goes to cross-border supplier payments: factories in China, Vietnam, Mexico.

Today, that $30 million runs through correspondent banking:

Wire fees: $35-50 per transaction. At 500 wires/year: $17,500-25,000.

FX spreads: Banks typically embed 2-4% above the mid-market rate, invisible in the quoted price. On $30 million, a 3% spread is $900,000.

Intermediary fees: SWIFT payments pass through multiple correspondent banks, each taking $15-25. Companies often gross up payments so suppliers receive the contracted amount—the sender absorbs this.

Settlement delay: 3-5 business days. Working capital trapped in transit.

**All-in: 3-4% of cross-border volume.**⁸ On $30 million, that’s $900,000-1.2 million per year disappearing into the banking system.

Now consider the alternative.

The company converts USD to USDC at par through Circle Mint. They send USDC to their supplier’s wallet. Settlement: minutes. Gas fees: negligible.

The supplier needs local currency—yuan, pesos, dong—not USDC. Someone has to convert it. Off-ramp costs vary by corridor: 0.3-0.5% for liquid markets like Mexico, 1-2% for Southeast Asia or Africa. Who bears this depends on commercial negotiation.

Scenario A: Supplier absorbs off-ramp costs. The sender’s cost drops to near-zero. The supplier’s effective receipt is reduced—but if off-ramp fees are lower than the lifting fees they were absorbing on incoming wires, they may come out ahead.

Scenario B: Sender absorbs off-ramp costs. The sender uses a service like BVNK or Bridge to deliver local currency directly to the supplier’s bank. The sender pays 0.5-1.5% depending on corridor.

Scenario C: Costs are negotiated. As stablecoin rails become standard, suppliers may offer discounts for faster settlement, sharing the savings.

Under the most conservative assumption (Scenario B):

Old cost: ~$900,000 (3% friction)

New cost: ~$300,000-450,000 (1-1.5% off-ramp fees)

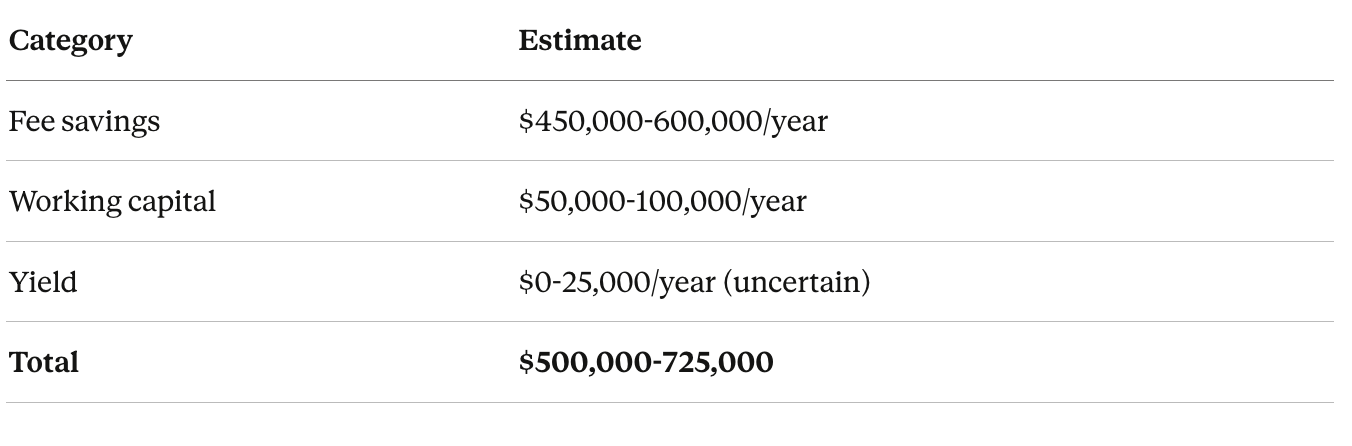

Annual savings: $450,000-600,000

And that’s before the working capital effects.

Working Capital

Fee savings are tangible. The velocity advantage may matter more.

With 500 international payments averaging $60,000 each and 3-5 day settlement times, this distributor has $400,000-600,000 trapped in transit at any given moment. Stablecoin settlement compresses that window from days to hours.

For a distributor operating at 5% EBITDA margins (typical for the industry⁹), redeploying $500,000 in previously trapped working capital means:

Inventory financing avoided: At 8-10% cost of capital, $40,000-50,000 annually.

Early-payment discounts captured: Many suppliers offer terms like “2/10 net 30”—pay within 10 days and take 2% off, or pay the full amount by day 30. This sounds trivial. It isn’t.

Think of it as a lending decision in reverse. By paying on day 30 instead of day 10, you’re keeping your cash for an extra 20 days but it costs you 2% to do so. That’s a 36% annualized rate.

Most companies understand this math. The problem is they don’t always have the cash on day 10. When your working capital is trapped in 5-day wire transfers, you might miss the discount window simply because the money hasn’t landed yet. Faster settlement means more chances to capture these discounts.

Treasury optionality: Cash on hand can earn yield in stablecoin products, though this benefit is in regulatory limbo. The CLARITY Act draft would prohibit exchanges from paying yield on balances.⁷ Yield capture is speculative; the working capital velocity benefit persists regardless.

Bottom Line

On $3.75 million EBITDA, that’s 13-19% improvement. From a treasury integration.

Why Now

Stablecoins have existed for years. Cross-border friction has existed for decades. Three things changed.

Legal clarity. Until mid-2025, stablecoins occupied a regulatory grey zone. No CFO experiments with legally ambiguous payment rails. The GENIUS Act, signed in July 2025, resolved that. Stablecoins are now a recognized payment instrument with clear reserve requirements.⁶

Off-ramp infrastructure. Two years ago, converting USDC to Vietnamese dong required navigating crypto exchanges with limited banking relationships. Today, turnkey providers handle it. Bridge, acquired by Stripe for $1.1 billion in early 2025, grew payment volume 10x in 2024 alone, reaching a $5 billion annualized run rate.¹⁰

Adoption is compounding. B2B stablecoin volumes surged from under $100 million monthly in early 2023 to over $3 billion by mid-2025. That’s 30x in two years.⁴ Deel has processed 125,000 stablecoin payouts across 100+ countries.⁵

For PE, this matters: a value creation lever that doesn’t require revenue growth, pricing power, or headcount reduction. Back-office infrastructure with front-office impact.

Objections and Responses

“Your suppliers won’t accept stablecoin payments.” Off-ramp providers like BVNK and Bridge receive stablecoins and deposit local currency to a supplier’s bank account within hours. The supplier doesn’t touch crypto; they just see pesos or yuan arrive faster than a wire.

“Your 1-1.5% cost assumption is too optimistic for some corridors.” Fair. Nigerian naira or Argentine pesos can hit 2-3%. But most industrial distributors concentrate payments in manufacturing hubs—China, Vietnam, Mexico—where infrastructure is maturing fastest.

“You’re shifting costs to suppliers, not eliminating them.” Partially true. But a Vietnamese factory receiving a wire through correspondent banking loses $15-25 in lifting fees plus days of float. If they off-ramp USDC for 0.5% and receive funds same-day, total system friction declines. The split is negotiable.

“What about volatility risk?” Stablecoins aren’t volatile. That’s the point. USDC is redeemable 1:1 for dollars. The exposure window is hours, not days. Circle is regulated, audited, and now public.

“Why hasn’t everyone done this already?” Because until mid-2025, there was no federal legal framework. CFOs at traditional companies don’t experiment with legally ambiguous payment rails. We’re now in the window where early adopters capture the savings while competitors wait.

The Investment Thesis

Private equity value creation has shifted. For decades, returns came from financial engineering and multiple expansion. In today’s rate environment, operational improvement is the primary lever. The firms that outperform will find inefficiencies others overlook.

Cross-border payment costs are one such inefficiency.

A mid-market distributor with $30 million in annual cross-border volume typically pays 3-4% in FX spreads, wire fees, and correspondent banking friction. Stablecoin rails can cut that by half or more. On a business running 5% EBITDA margins, that’s 10-15% of operating profit recovered. From a back-office integration.

Most companies treat this as fixed. It isn’t.

The savings flow directly to EBITDA. No revenue risk. No customer behavior change. No dependency on technology that hasn’t yet found product-market fit.

At Inversion, we acquire companies where this lever applies and integrate stablecoin infrastructure as part of the value creation plan. For businesses with meaningful cross-border exposure, the impact is 13-19% EBITDA improvement. Top-quartile operational alpha from a back-office integration.

The market continues to debate whether stablecoins will displace consumer payment networks. That may happen eventually; it won’t happen soon. The more immediate opportunity is in B2B: $25 trillion in annual payments moving through infrastructure built for a different era.

Entire industries were transformed by just-in-time manufacturing - the insight that inventory sitting idle is waste. The same logic applies to money. Capital trapped in 5-day settlement windows is working capital that isn’t working.

Stablecoins enable just-in-time money. That’s the alpha.

Notes

¹ Scott Fearon, Dead Companies Walking (St. Martin’s Press, 2015), p. 37.

² Swipesum, “Visa vs Mastercard (2025),” November 2025.

³ WalletHub, “How Much Does Costco Pay Visa?,” January 2022; View from the Wing, April 2015.

⁴ Artemis, Castle Island Ventures, and Dragonfly, “Stablecoin Payments from the Ground Up,” June 2025.

⁵ BVNK case study, “Deel teams up with BVNK to pioneer instant payments,” 2025.

⁶ Mayer Brown, “GENIUS Act Signed into Law,” July 18, 2025.

⁷ Latham & Watkins, “US Crypto Tracker Legislative Developments,” January 2026.

⁸ BVNK, “Blockchain in cross-border payments: a complete 2025 guide,” October 2025.

⁹ National Association of Wholesaler-Distributors, 2023.

¹⁰ Architect Partners, “Stripe is acquiring Bridge for $1.1 billion,” October 2024; Payments Dive, October 2024.

Let’s gooo!

Outstanding breakdown of how payment friction gets buried in COGS as fixed costs. The early payment discount math (36% annualized) really exposes the hidden cost of slow settlement. From my own experiance in ops, treasury teams rarely scrutinize these bleeds bc they seem immovable. The working capital velocity angle is where this gets intresting, especially for companies already stretched thin on inventory financing.