Why Tokens Can’t Compound

Equity compounds. Tokens don't.

I am writing this as crypto is melting down. Bitcoin touched $60K, Solana is back to FTX estate sale levels, and Ethereum is $1,800. I’ll spare you the permabear talk.

This post is about something more fundamental: why tokens can’t compound.

Prices will recover from here. I’ll be called a grave dancer. The core argument will get buried in volatility. But let’s go.

Over the past months I’ve argued (at risk of being called midcurve) that crypto is overpriced on fundamentals, that Metcalfe’s Law doesn’t justify valuations, and that adoption and prices can diverge for years.

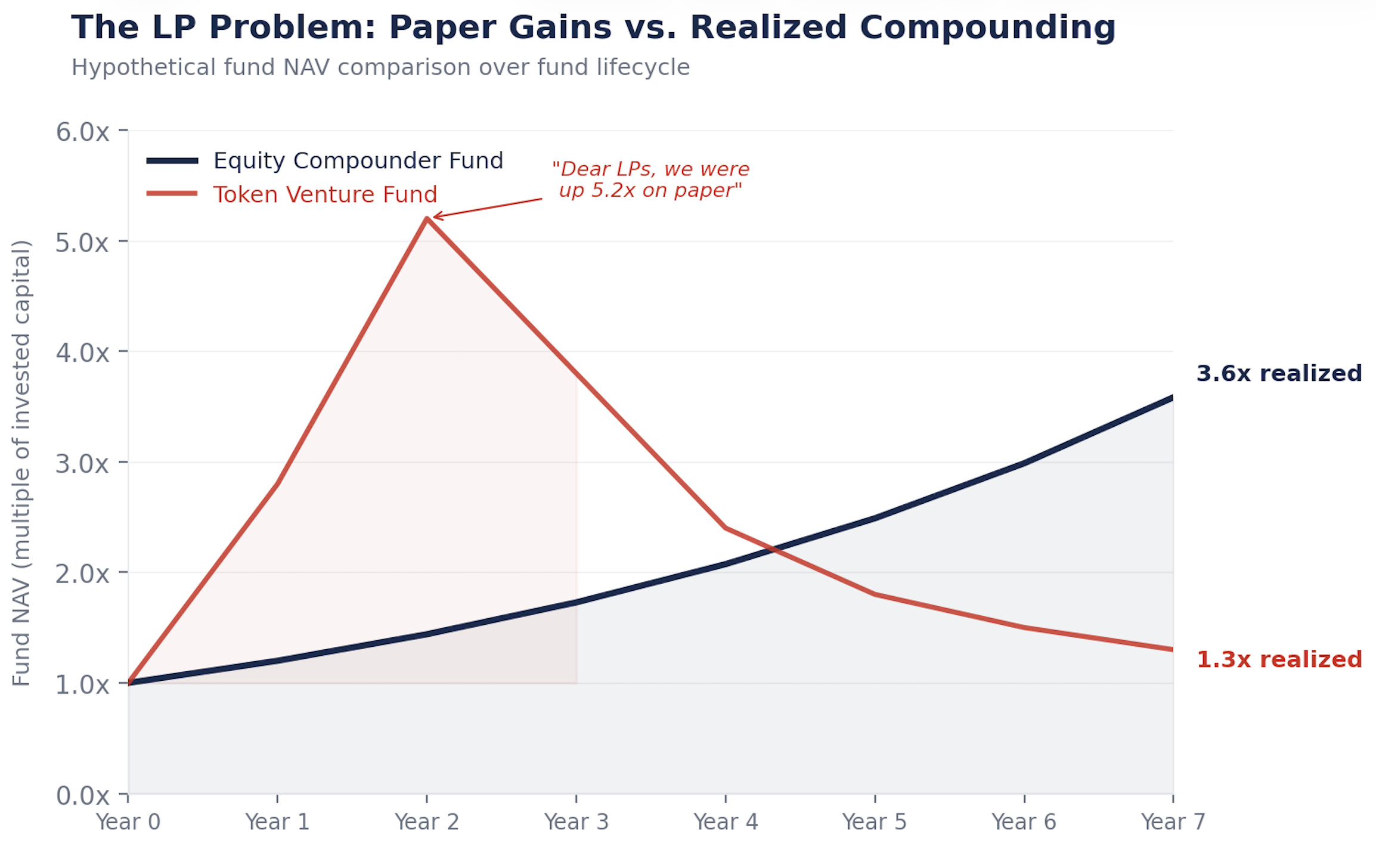

“Dear LPs, stablecoin volume grew 100x but our returns were 1.3x. Thank you for your trust and patience.”

The strongest pushback across all of them?

“You’re being too bearish. You don’t understand what tokens represent. This is a new paradigm.”

I understand exactly what tokens represent. That’s the problem.

The Compounding Machine

Berkshire Hathaway is worth ~$1.1 trillion. Not because Buffett timed it perfectly. Because it compounds.

Every year, Berkshire takes its earnings, reinvests them into new businesses, expands margins, acquires competitors, and grows intrinsic value per share. The price follows. Eventually, inevitably, because the underlying economic engine gets bigger.

This is what equity does. It is a claim on a reinvestment engine. Management takes profit. Allocates capital. Buys growth. Cuts costs. Retires shares. Every good decision compounds into the next.

$1 compounding at 15% for 20 years = $16.37.

$1 compounding at 0% for 20 years = $1.

Equity turns a dollar of earnings into sixteen. Tokens turn a dollar of fees into a dollar of fees.

Show Me the Machine

Here’s what happens inside a PE fund when we acquire a business generating $5M in free cash flow:

Year 1: $5M FCF. Management reinvests: R&D, stablecoin treasury rails, debt paydown. Three decisions.

Year 2: Each decision pays off. FCF: $5.75M.

Year 3: Those gains compound into the next round of decisions. FCF: $6.6M.

That’s a business compounding at 15%. The $5M became $6.6M not because the market got excited. It happened because a human made capital allocation decisions that each fed into the next. Do that for 20 years and $5M becomes $82M.

Now here’s what happens inside a protocol generating $5M in fees:

Year 1: $5M in fees. Distributed to token stakers. Gone.

Year 2: $5M in fees. Maybe. If users come back. Gone.

Year 3: Depends on whether the casino is full.

Nothing compounds. There is no Year 3 flywheel because there was no reinvestment in Year 1. Grant programs are not enough.

Tokens Were Designed This Way

This wasn’t an accident. It was a legal strategy.

Go back to 2017-2019. The SEC was hunting anything that looked like a security. Every lawyer advising a protocol team said the same thing: do not make this token look like equity. No cash flow claims. No governance over the Labs entity. No retained earnings. Frame it as utility, not investment.

So the industry built tokens to be explicitly not-equity. No claim on cash flows. Avoids looking like a dividend. No governance over Labs. Avoids looking like shareholder rights. No retained earnings. Avoids looking like a corporate treasury. Staking rewards framed as network participation, not yield.

It worked. Most tokens avoided securities classification. They also avoided being anything that compounds.

The entire asset class was deliberately engineered to not do the one thing that creates long-term wealth.

The Labs Keeps the Equity. You Hold the Coupon.

Every major protocol has a for-profit Labs entity sitting next to it. The Labs builds the software, controls the frontend, owns the brand, and captures the enterprise relationships. The token holders? They get governance votes and a floating claim on fees.

The pattern is the same everywhere. Labs gets the talent, the IP, the brand, the enterprise contracts, the strategic optionality. Token holders get a floating-rate coupon on network usage and the privilege of voting on proposals that Labs increasingly ignores.

No surprise. When someone acquires a protocol ecosystem, as Circle did with the Axelar team, they buy the Labs equity. Not the token. Because equity compounds. The token doesn’t.

Regulation without intention creates perverse outcomes.

What You Actually Own

Strip away the narrative. Strip away the price volatility. Look at what a token holder actually receives.

When you stake ETH, you get ~3-4% yield. That yield is a function of the network’s inflation schedule, adjusted dynamically by staking rate. More stakers, lower yield. Fewer stakers, higher yield.

That’s a floating-rate coupon tied to a protocol-defined schedule. That’s not equity. That’s a bond.

Yes, ETH can go from $3,000 to $10,000. But a junk bond can double if spreads compress. Doesn’t make it equity.

The question is: what is the mechanism through which your cash flow grows?

Equity: management reinvests and compounds. Growth = f(ROIC × reinvestment rate). You participate in an expanding economic engine.

Tokens: cash flow = f(network usage × fee rate × staking participation). You receive a coupon that fluctuates with demand for blockspace. There is no reinvestment mechanism. No compounding engine.

Price volatility makes people think they own equity. The economic structure says they own fixed income. With 60-80% annualized vol. That’s the worst of both worlds.

Most tokens: 1-3% real yield after inflation dilution. No fixed-income investor on earth would accept that risk-return profile. But high volatility in these instruments will always attract a new set of buyers. The greater fool theory at play.

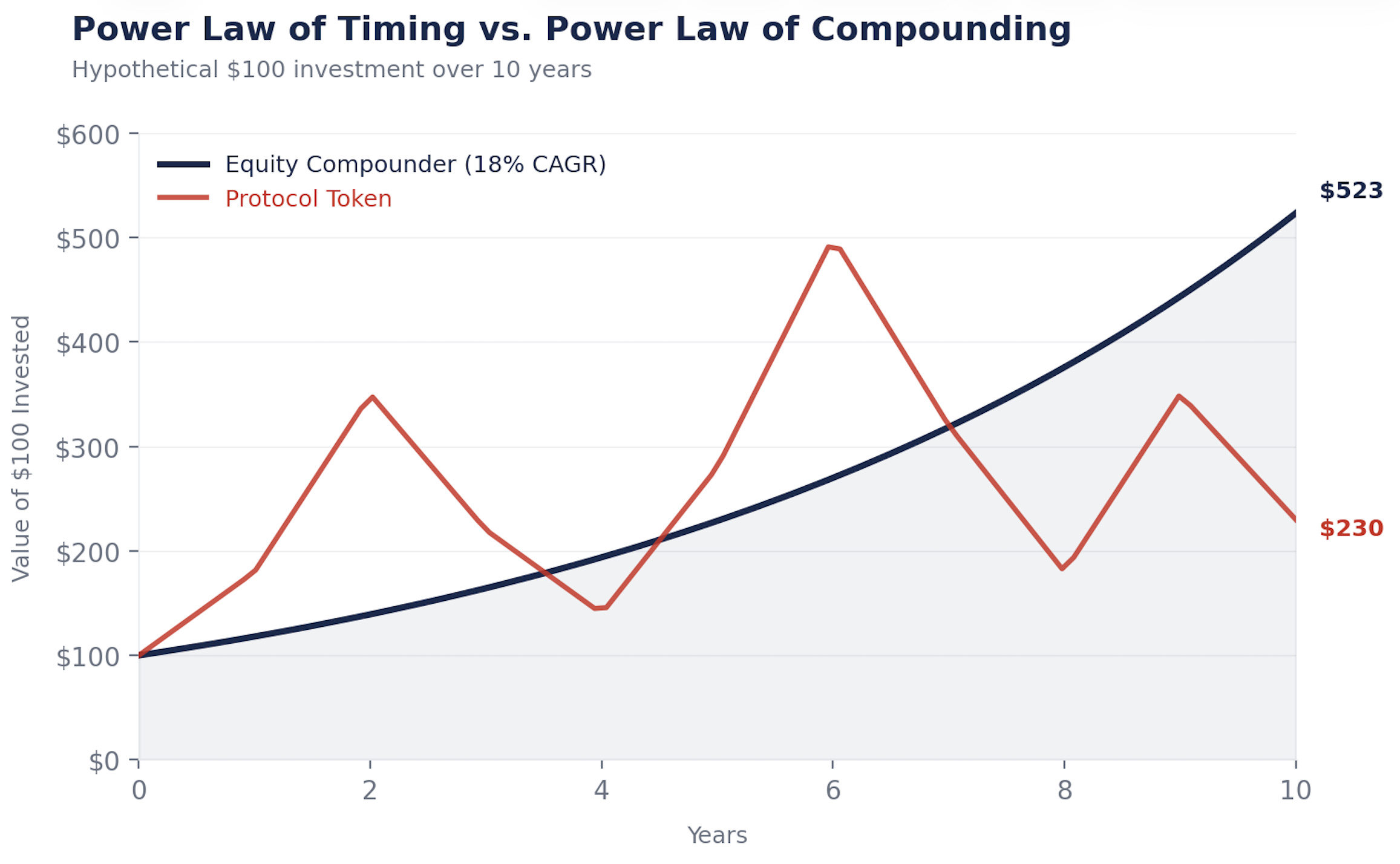

Power Law of Timing vs. Power Law of Compounding

This is why tokens, at least in their current form, will not accrue value and compound. The market is realizing this is the case. It is not dumb and it is shifting to crypto-linked equities. First DATs (more on that below) and increasingly to companies that are using this technology to lower costs, increase revenues and compound.

Crypto wealth creation follows a power law of timing. The people who got rich bought early and sold at the right moment. My own portfolio follows this pattern. We call it liquid venture for a reason.

Equity wealth creation follows a power law of compounding. Buffett didn’t time Coca-Cola. He bought it and let it compound for 35 years.

In crypto, time is your enemy. Hold too long and gains evaporate. High inflation curves, low float and high FDV mechanics, and little demand and too much blockspace play a big part in this. Hyperliquid is a notable exception.

In equity, time is your ally. The longer you hold a compounder, the more the math works.

Crypto rewards traders. Equity rewards owners. There are far more rich owners than rich traders.

I run these numbers because I have to. Every LP asks: “Why not just buy ETH?”

Pull up a compounder. Danaher, Constellation Software, Berkshire. Now pull up ETH. The compounder grinds up and to the right because the engine gets bigger every year. ETH spikes, crashes, spikes, crashes. The cumulative return depends entirely on when you entered and exited.

Both charts might end in the same place. But one lets you sleep at night. The other requires you to be a prophet. Time in the market beats timing the market. Everyone knows this. The problem is actually staying in the market. Equities make that easier: cash flows put a floor under the price, dividends pay you to wait, and buybacks compound while you hold. Crypto makes it brutal. Fees dry up, narratives shift, and there is nothing to fall back on. No floor. No coupon. Just conviction. HODL.

I’d rather be an owner than a prophet.

The Trade

If tokens can’t compound, and compounding is what creates wealth, then the conclusion writes itself.

The internet created trillions of dollars of value. Where did it end up? Not in TCP/IP. Not in HTTP. Not in SMTP. These protocols are public goods. Enormously valuable, zero investable return at the protocol layer.

The value went to Amazon, Google, Meta, Apple. Companies that built on the protocols and compounded.

Crypto is rhyming.

Stablecoins are becoming the TCP/IP of money. Enormously useful. Widely adopted. The protocols themselves may or may not capture proportional value. Tether is a company with equity, not a protocol. There’s a lesson in that.

The companies that plug stablecoin rails into their operations, reducing payment friction, improving working capital, cutting FX costs, those are the compounders. A CFO who saves $3M/year by switching cross-border payments to stablecoin rails can redeploy that $3M into sales, product, or debt paydown. That $3M compounds. The protocol that facilitated the transfer earned a fee. It did not compound.

The fat protocol thesis argued crypto protocols would capture more value than the application layer. Seven years later, L1s make up ~90% of market cap but their fee share collapsed from ~60% to ~12%. Apps generate ~73% of fees but represent less than 10% of valuation. Markets are efficient.

The market continues to hold on to this fat protocol mantra. The next chapter in crypto will be defined by crypto-enabled equity. Businesses that own users, generate cash flow, and have management teams that implement crypto to improve their business and compound at a higher rate. Those businesses will outperform tokens by a country mile.

Robinhood, Klarna, NuBank, Stripe, Revolut, Western Union, Visa, Blackrock. This basket outperforms a basket of tokens.

These businesses have real floors. Cash flows, assets, customers. Tokens don’t. And when tokens are trading at exorbitant multiples on future revenues, the downside is brutal.

Long the technology. Selective on tokens. Very long the equity of businesses that compound the advantages this infrastructure creates.

The Uncomfortable Part

Everyone trying to fix this is accidentally proving the thesis.

DAOs that attempt real capital allocation (MakerDAO buying Treasuries, creating SubDAOs, appointing domain teams) are slowly reinventing corporate governance. The more a protocol tries to compound, the more it has to look like a company.

DATs and tokenized equity wrappers don’t solve it either. They create a second claim on the same cash flows that competes with the underlying token. The wrapper doesn’t make the protocol better at compounding. It just redistributes economics from token holders who don’t hold the DAT to those who do.

Burns are not buybacks. ETH’s burn is a thermostat set to one temperature. Apple’s buyback is a human reading the weather. Intelligent capital allocation, the ability to change strategy based on conditions, is what compounds. Rules don’t compound. Decisions do.

And regulation? It’s actually the most interesting part. Tokens can’t compound today because protocols can’t operate as businesses. Can’t incorporate, can’t retain earnings, can’t make enforceable commitments to token holders. The GENIUS Act proved Congress can bring tokens inside the financial system without killing them. The day we get a framework that lets protocols operate with the capital allocation tools of a corporation, that’s the biggest catalyst in crypto’s history. Bigger than ETFs.

Until then, smart capital flows to equity. And the compounding gap grows wider every year.

None of This Is Bearish on Blockchains

I want to be clear about something. Blockchains are economic systems. They are incredibly powerful and they will be the rails of digital payments and agentic commerce. We are building a chain at Inversion because we believe that deeply.

The technology is not the problem. The token economics are the problem. Networks today pass value through instead of compounding it. That will change. Regulation will evolve. Governance will mature. Some protocol will figure out how to retain and reinvest value the way a great business does. When that happens, tokens become equity in all but name. And the compounding machine turns on.

I’m not betting against that future. I’m betting on the timing.

There will come a day when networks compound value. Until that day comes, I will buy businesses that compound faster with crypto.

I could be wrong on timing. Crypto is an adaptive system and I think that is one of its most valuable properties. But I don’t need to be perfectly right. I just need to be directionally right that compounders outperform over time.

And that is the beauty of compounding. As Munger put it, “It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.”

Crypto made infrastructure cheap. The wealth will go to those who use that cheap infrastructure to compound.

The internet taught us this lesson twenty-five years ago.

Time to act on it.

Invert.

- Santiago

We enjoyed reading this 👏

The core assumption underneath your piece is that compounding has to come from cash flows being reinvested by a central allocator. That’s how companies compound, and you’re absolutely right about that. But crypto gives us another design space that hasn’t really been explored yet.

The reason we think this distinction matters is that most attempts to “fix” tokenomics over the last cycle stayed inside the same frame. Tweaks to fee splits, burns, buybacks, ve-models, or pseudo-treasuries all assume value must be captured and redistributed financially. We came at the problem from a different angle, asking what it would look like if compounding happened through how quickly systems agree and execute, rather than through cash flows.

Reality is being built as a permissionless protocol that takes Bitcoin’s core idea and extends it beyond money into software, data, and markets. We’ve spent a lot of time studying the last 15 years of tokenomics, and the pattern is pretty consistent. Most systems end up being extractive. Usage turns into fees, fees get distributed, and the system resets. Value moves through the network, but it doesn’t accumulate inside it.

We designed Reality around a different set of principles, closer to generative economics than fee extraction. More like food co-ops or employee-owned companies than platforms selling access.

Reality apps, or rApps, don’t pay per transaction. They reserve throughput by locking $NET. That small shift changes the entire loop. Instead of usage producing fees, usage pulls supply out of circulation. As more rApps grow, more $NET gets locked. Participation density increases. Coherence improves. Finality gets faster. Speed feeds back into more usage.

Where your analysis looks for compounding in cash flows, Reality compounds in state. The mental shift for us was to stop thinking about $NET as revenue at all. In practice, it functions more like a claim on future coordination capacity. As rApps scale, they reserve more of that capacity in advance. The network ends up doing more work per unit of time as usage grows.

One way to translate this into your frame is to think of time as the surplus being reinvested. In companies, surplus shows up as cash that gets allocated. In Reality, surplus shows up as time saved. As more independent nodes participate, the network reaches agreement faster and finalizes earlier. That saved time isn’t distributed. It immediately turns into higher throughput and faster execution. The system compounds by doing more useful work per unit of time as usage grows.

You wrote that there’s no Year 3 flywheel because there was no reinvestment in Year 1. That’s true for fee-based systems. In Reality, Year 1 usage locks supply. Year 2 starts with more capacity already reserved. Year 3 starts faster than Year 2. Nothing gets reinvested as cash. The system reinvests by becoming more efficient.

Reality compounds by reinvesting time saved into more work, rather than reinvesting cash into more assets.

Your description of ETH staking is spot on. It behaves like a floating-rate coupon. In Reality, there’s no yield for holding. Supply gets removed because the network needs it to function. Value accrues through scarcity tied to usage rather than through coupons or dividends. A closer mental model is spectrum licenses or cloud capacity reserved ahead of time.

We agree with your broader point that most protocols today are public goods with little or no return. Reality is designed so the public good itself becomes more efficient as it’s used. That efficiency tightens supply, and that tightening reflects back into the token. There’s no treasury allocating capital and no management making discretionary decisions. Coordination itself is what compounds.

You wrote that some protocol will eventually figure out how to retain and reinvest value the way a great business does. That’s the direction we’re exploring at Reality 🫡

If anyone’s interested in the underlying mechanics, we wrote more about it here:

https://realitynetwork.substack.com/p/tokenomics-part-3-when-money-stops

Most accurate article I’ve ever read. Shaped in words what I have been thinking for years now, but couldn’t explain this well. Bravo sir!

Can I anyhow contribute to this?