Yield and Uncertainty

If you don't know where the yield is coming from, you're the yield.

Why do SaaS stocks keep getting crushed even after 50-60% drawdowns?

It’s yield. It’s always yield.

This isn’t a SaaS story. It’s a story about what happens when technology introduces real uncertainty into an asset class in an environment where everyone is a SaaS expert prompting Claude. Algos are in control and they respond to yield.

Let me give you an inside scoop into the calculus to cut a position in today’s world:

Bloomberg Headline: AI is replacing SaaS at a record pace…

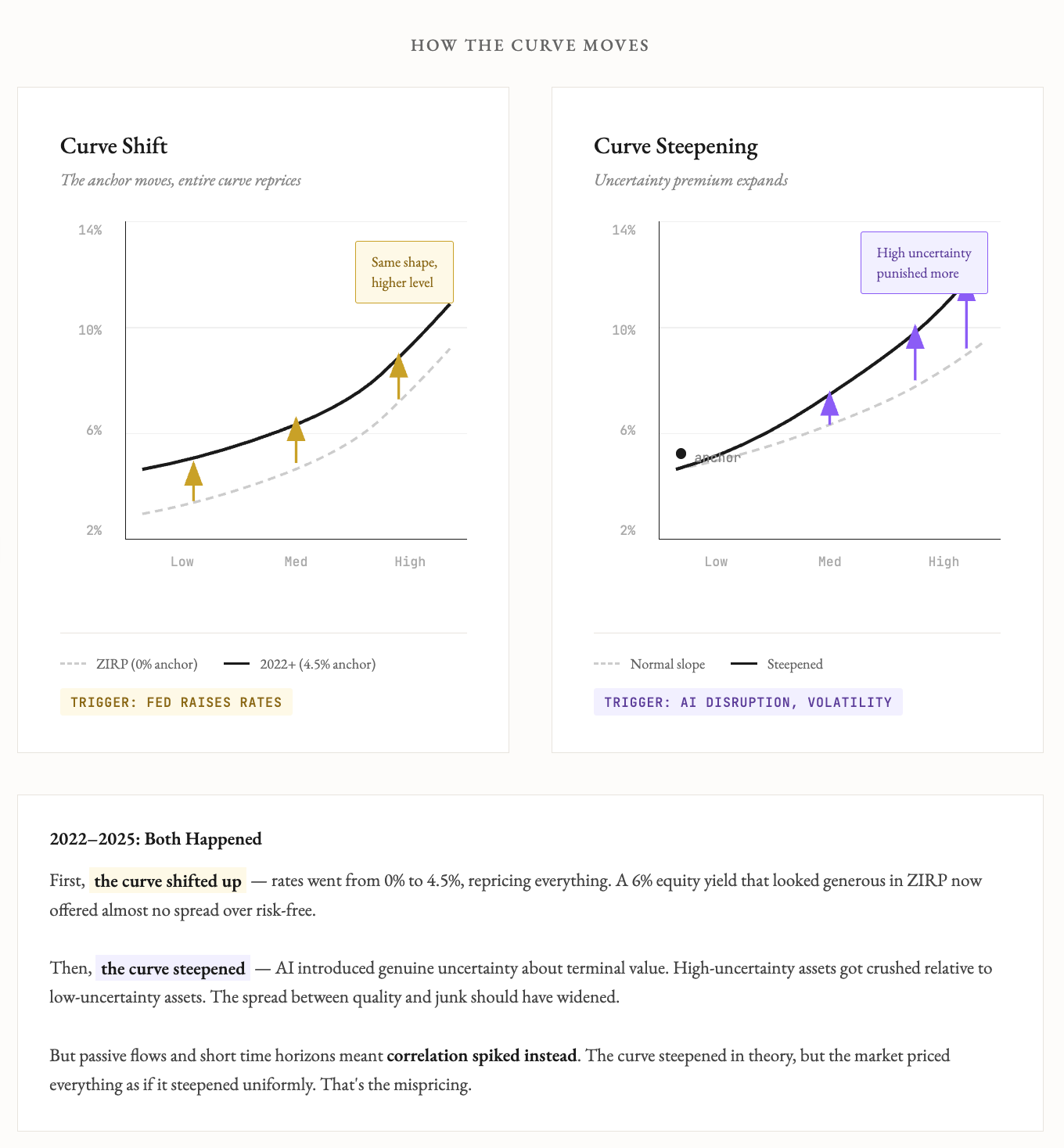

Algo reads: more risk and uncertainty in SaaS. The risk curve steepens (right side).

Math: give me FCF yield of all SaaS. Cut growth consensus by half.

Instruction: cut lowest names where FCF < T-bill.

That’s what happens when technology introduces more risk in a sector. An entire repricing. Correlation within the sector increases when everything is chopped.

Intuitively it makes sense if you believe the entire SaaS sector just got more risky because of AI disruption risk.

Bear markets sharpen the mind.

Headline 2: FCF is understated. Many SaaS companies have massive SBC.

Quant: adjusts FCF Yield for SBC. Then runs same script to cut too much risk in book.

Another 20% leg down.

Metrics are shorthand. You may be sitting there saying, wait a minute…if this is what is happening and quality is being sold with trash, then let me prompt AI to create a model:

Claude: build me a model that spots durable SaaS businesses that meet this criteria:

Consistent 5Y ARR growth

Low churn

>70% EBITDA margin

System of record

Little SBC

Show me highest FCF yield assuming 5Y ARR growth

Buy cheap

I used to be a SaaS analyst back in the day. I am not technical enough to understand to what degree SaaS will be replaced by AI. What I can tell you is that some of these businesses are deeply entrenched. It’s hard to replace software you need to be compliant, software you’re trusting with mission-critical stuff.

This may not age well, but I don’t need to be perfectly right. My mental model for AI is that data and the rails to transact data are becoming more critical for AI to be useful. Anything that has a strong data moat will survive and become more critical. AI will make those businesses more, not less valuable.

One investor summarized this well: “On the ‘software is dead’ narrative: my intuition is that AI makes strong software companies stronger and weak software companies weaker. This is because the moat of strong software companies was never software, but rather distribution, proprietary data, workflow integration, enterprise lock-in, network effects, trust and compliance, etc.—whereas the moat of weak software companies was just… software.”

I couldn’t agree more.

Luddites and techno-optimists make the same mistake: they are too extreme. AI is amazing but it will not replace everything in the stack.

I saw a glimpse of AI disruption a decade ago with SaaS data visualization companies like Tableau. The first data vis company was useful. The tenth was not. The visualization layer was commoditized and value shifted to data insights. You saw a commoditization of wrappers real fast. Back then you didn’t need AI to see the truth, you simply had to understand: data wrappers are not as valuable, insights are more valuable. The first startup creates value; the tenth not so much. Competition is for losers. You were better off buying businesses that used these tools to improve business decisions, not the vendor themselves. Unless churn was low. If you could ask for only one data set it’s this: raw file of every customer with monthly spend. Companies make all sort of adjustments to churn when reporting but they can’t hide behind the raw data.

So What Survives?

AI presents real questions as you do diligence for SaaS.

Data gravity. When switching costs are measured in years and millions of dollars of implementation risk, when the data itself is the moat, when regulators require auditability only the incumbent provides. That’s a system of record.

Workday owns your payroll history. ServiceNow owns your IT workflows. HubSpot owns your marketing emails.

One of these things is not like the others.

The market is treating them the same. That’s the mispricing.

Three AI Scenarios to Stress-Test

1. AI commoditizes the application layer.

Klarna claimed AI could do the work of 700 customer service agents and replaced Salesforce with internal tools. Is Klarna representative of the rest? What to look out for: churn. How to verify: channel checks. Talk to businesses of varying sizes. Note that Klarna later reversed course and started hiring humans again after customer satisfaction declined. A cautionary tale about moving too fast.

2. AI eliminates the user.

Agents don’t need human-friendly UIs. The per-seat model assumes humans in the loop. What if they’re not? What to look out for: pricing model changes and contract value (KPIs: pricing menus on sites, dollar retention, average contract value).

3. Value shifts to data and infrastructure.

The SaaS wrapper becomes commodity. What survives: proprietary data and the pipes underneath. What to look out for: I hate the word “proprietary” because it means everything and nothing. It’s lazy. What about the data makes it essential and locked in. Hard to port over? Can businesses rip their CRM and plug it into their own custom build?

Some businesses die here. Some don’t.

If you came for answers on whether to buy SaaS here or not, sorry. I’m too busy looking at businesses that have already been left for dead. Where it doesn’t take much to revitalize them.

Since last year I have been risk off because I think nothing is very cheap, and when things are not cheap (multiples are high → yield is low or lower than risk-free) I don’t think it’s a good setup to be far out on the risk curve. So no, I am not compelled to do a lot of work on SaaS. The repricing is warranted because there is more uncertainty.

The point I’m making is that someone will make a killing here:

The market is not appreciating that most SaaS is meeting or beating plans. Irrational partly, but some truth that the market is discounting more uncertainty on growth, which is warranted. The nuance is how much more uncertainty.

The Math That Kills You

A SaaS stock at 25× FCF yields 4%. Treasuries yield around 4.2%. Why own the stock?

Oh wait…but now adjusting for SBC that yield goes down to 2% vs 4.2% risk-free? Do I really believe it will keep growing? Conviction gets tested really fast when the stocks go down.

SBC goes unnoticed or is celebrated as a feature, not a bug, in bull markets. It’s rat poison in bear markets. The truth is somewhere in the middle.

SBC allows the company to attract and retain talent without burning cash. The “true” cost of SBC is somewhere between reported FCF and SBC-adjusted FCF. The market goes to either extreme.

SBC can help align incentives, making employees owners; a subtle but powerful incentive mechanism that doesn’t show as clearly in the financials but matters a lot for business performance. I wouldn’t want to own a company where the employees are not owners. It’s a classic principal-agent problem.

Back to summarizing this article because it’s 8:30am and I have one hour to prompt Claude to find me deep fucking value.

Always remember: am I getting paid enough? The yield framework is a useful starting point, not the conclusion.

You’re sitting there crunching numbers and prompting, and come across this:

Amex yields 7% and ServiceNow yields ~2.6%. Buy Amex, sell ServiceNow.

Not so fast. If markets were genuinely mispriced, arbitrageurs would close the gap. The market is telling you something: either Amex has hidden risks (credit cycle, regulatory, fintech disruption) or ServiceNow has hidden value (growth duration, pricing power, switching costs).

When the math looks easy, you’re probably missing something. The market isn’t that stupid.

However, it is a wonderful time in the market because it is having a pretty interesting dislocation trying to figure out how real the AI disruption risk is. It is also interesting because growth is being discounted and when you’re farther out on the risk spectrum, it doesn’t take much to derail your thesis.

If you need SaaS to compound at 20-30% a year just to get paid, you’re far more exposed to technological risk, to execution risk, to everything that can go wrong over a long duration.

If you’re getting paid 1% for owning more uncertainty and uncertainty rises, that is very expensive relative to other things.

When Spreads Compress

When spreads compress against risk-free, you have to believe a lot. Right now the market is believing much less for most SaaS. AI introduced real uncertainty about survivability and terminal value. Combined with passive flows and impatient capital, it’s a recipe for disorderly repricing.

Here’s what’s strange: when dispersion in quality should be growing, we’re seeing the opposite. Correlation among SaaS names is spiking. The market is chopping everything - systems of record and wrappers alike - as if they’re the same.

They’re not.

I tell my team: assume the market is always right and prove me why it’s not. But when passive flows dominate and algos run the show, prices can stay wrong longer than they should.

Bear markets return stocks to their rightful owners. I am tempted to dust off my SaaS notes from a prior life if things continue to bleed. There will be generational opportunities here.

To Tie It All Together

The market is usually not wrong, but sometimes it is very wrong as it processes new information.

AI introduced more uncertainty to SaaS.

The market is working through that, and we won’t know easily who’s right.

It feels messy and disorderly, and that is when active management matters. This is where fat pitches come.

Simple shorthand frameworks like yield-on-risk are useful only to screen inconsistencies and mispricings. But they do not fundamentally answer some of the more qualitative things: What is the quality of the business? What do I need to believe for this thing to keep growing and compounding at the same or higher rate? Is ServiceNow the same as Monday.com? The model will tell you what you want.

Categorically, I’d rather buy stuff where I need to believe less to get paid. You’ll find people that believe systems of record will grow more, not less, because of AI, and the selloff is a generational entry point. Others believe the opposite.

The market pendulum swings to extremes while business fundamentals don’t deviate that much. That spread will always allow for excess returns.

The Bigger Picture

SaaS won’t be the last sector to see this.

We’re heading into a decade of uncertainty, fueled by an accelerating pace of technological creative destruction. AI will run through every sector where software mediates value. Crypto will do the same for financial services, especially the infrastructure layer. Stablecoins alone threaten a significant chunk of annual cross-border payment fees; global corporations pay an estimated $120 billion annually in these transaction costs. The incumbents collecting those tolls will not have a soft landing.

But some businesses will be immune to disruption. Not because they’re technologically superior, but because humans never change. People will still swipe credit cards. They’ll still need payroll. They’ll still get sick and file insurance claims.

The businesses closest to unchanging human behavior are the ones with the most durable yields.

The Part Most People Will Get Wrong

There is no shorthand for doing the work.

You cannot easily prompt your way to alpha. “Find me stocks with high FCF yield adjusted for SBC, durable moats, low capex, and minimal AI disruption.” That prompt does not generate alpha. Not because the models are bad. Because the models are trained on the same public information everyone else has.

Garbage in, garbage out.

AI makes information aggregation a commodity. It lowers the skill floor for building models, pulling data, running screens. Those screens are getting better. But they’re incomplete because they can only see what’s already online.

The edge shifts to what AI can’t do: talking to customers, talking to competitors, walking the factory floor, reading body language in a management meeting. Primary research. The analog stuff that doesn’t exist in a training set.

Markets will converge on some consensus truth, and not question it. Capital is sitting in passive indexing. Nobody gets paid to ask whether the consensus is wrong. The algos aren’t doing channel checks. They’re trading momentum and mean reversion on the same data everyone else sees.

That’s the inefficiency. Not the data. The judgment.

This Is the Age for Active Management

Not because passive is broken. Because the combination of technological disruption, passive dominance, and algorithmic trading creates a specific kind of mispricing: consensus trades that nobody stress-tests.

When correlation spikes and dispersion should be expanding, that’s when deep understanding of individual businesses matters most. You’re seeing this play out in SaaS.

If you’re buying equities in a sector facing technological uncertainty, know what you’re actually earning after dilution. Know what has to go right. Know what kills you if it doesn’t.

And know that the answer won’t come from a screen.

If you don’t know where the yield is coming from, you’re the yield.

—Santiago

You are genuinely the best analytical team in the new economy. Wished i had been more cautious! Tx. Ludo